Against the backdrop of a global economic downturn, how to reduce costs and improve efficiency has become a core concern for game industry practitioners. Compared with fierce competition in traditional user acquisition channels such as product development and advertising marketing, an increasing number of mature game developers have begun to shift their attention to transaction and payment links that are directly related to corporate revenue, seeking to reduce reliance on high commissions charged by distribution channels.

With the rise of performance-based distribution models and the advancement of antitrust regulation, policies of major platforms such as Apple and Google have gradually loosened, providing opportunities for the development of third-party payment solutions for game companies. Leading game companies such as Supercell, Warner Bros., and Scopely have successively begun to build official website payment systems, offering players top-up services through self-built official websites so that more revenue can be retained within the company rather than paid to channels as commissions.

Although official website payment also constitutes a form of third-party payment outside of game distribution channels, it differs from the previously tightly regulated practice of “payment switching.” Payment switching usually includes two models: one involves replacing the in-game payment channels with self-operated payment channels through package updates after the game is listed, thereby bypassing the payment methods reviewed and approved by Apple/Android distribution channels; the other involves displaying and guiding players within the game to third-party recharge pages for payment. Official website payment does not necessarily involve directly guiding players to recharge within the game. Instead, it more often provides players with an official and secure recharge channel outside the game.

If game companies can strictly comply with platform regulatory requirements, the official website payment model still has considerable practical room for operation. In this regard, we have summarized platform regulatory policies and key compliance points for official website payment to help game companies maximize revenue while complying with the rules.

Regulatory Policies of Apple and Google Play on Third-Party Payments

With respect to third-party payments, Apple App Store and Google Play have long maintained relatively strict regulatory stances.

Since 2017, Apple has clearly stated in the App Store Review Guidelines that, except for special authorization in the United States, apps and their metadata must not include buttons, external links, or other calls to action that direct customers to use purchasing mechanisms other than in-app purchases. Apple reserves the right to remove apps that guide payments from the App Store or terminate developer accounts.

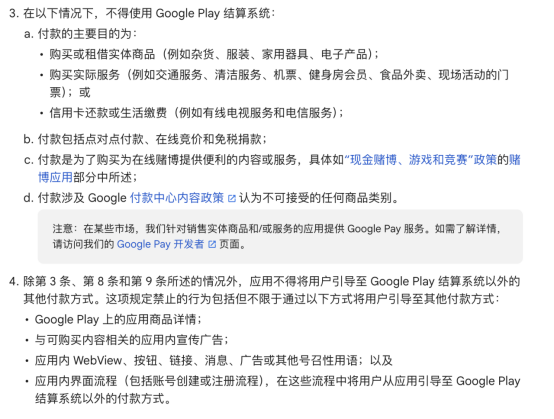

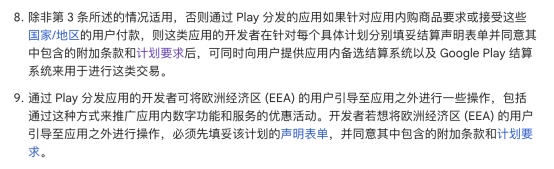

Google Play has similarly stipulated in its Developer Program Policies that, except for special payment purposes where the Google Play billing system is not required, or where alternative in-app billing systems are permitted in specific countries or regions, apps must not direct users to payment methods other than the Google Play billing system.

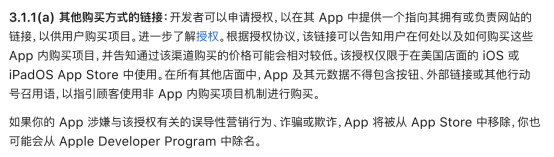

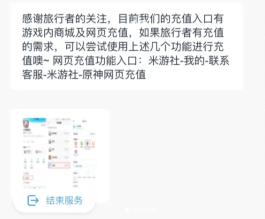

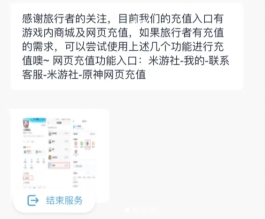

In August 2023, two third-party payment solutions launched successively by miHoYo were both restricted by Apple. The first involved embedding a recharge redirection interface in the form of customer service links within the fan community app “Miyoushe” (see Figure 1), which was soon removed from the Apple App Store. The second involved launching the miHoYo Payment Center mini program on Alipay, which became unavailable in iOS Alipay only two weeks later (see Figure 2).

Figure 1

Figure 1

Figure 2

Figure 2

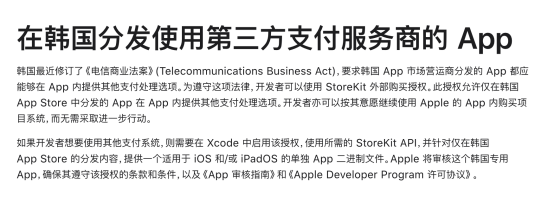

However, with the continuous advancement of antitrust regulatory processes in various regions, both Apple App Store and Google Play have made certain policy adjustments, gradually loosening restrictions on third-party payments in regions such as South Korea, the United States, Europe, and Japan.

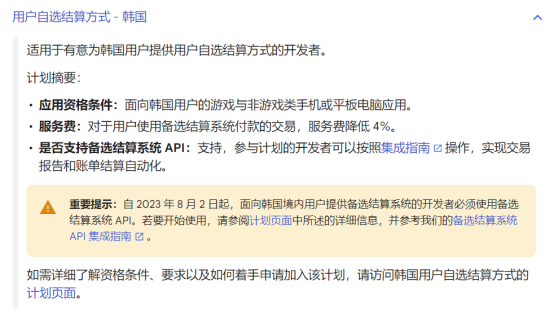

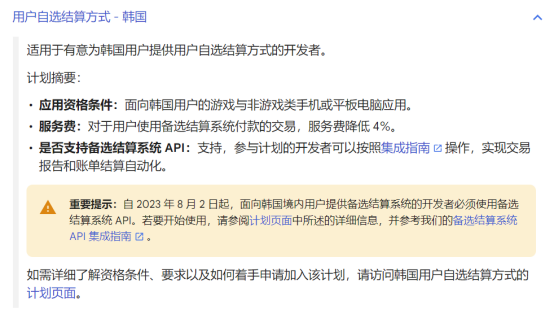

1. South Korea

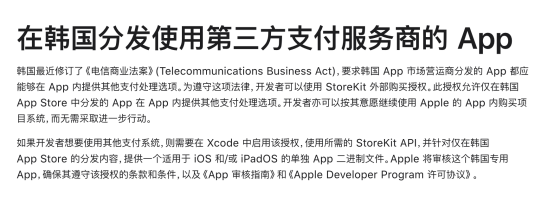

On August 31, 2021, the Korean National Assembly passed the Enforcement Decree of the Telecommunications Business Act. Annex 4, Article 8 updated the definition of unfair conduct by app stores, including refusing, delaying, or restricting the use of payment methods other than designated payment systems. South Korea became the first country to require app stores to allow apps to integrate third-party payment systems.

Against this backdrop, Apple allows Korean developers to offer third-party payment systems, subject to application, monthly sales reporting to Apple, and a 26% commission charged by Apple.

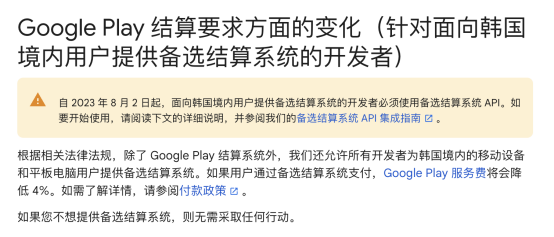

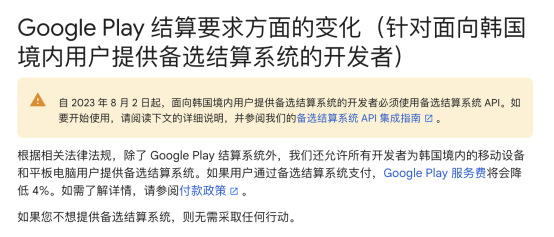

Google has also opened alternative billing systems to Korean developers, reducing service fees by 4%, but similarly requiring prior application.

2. United States

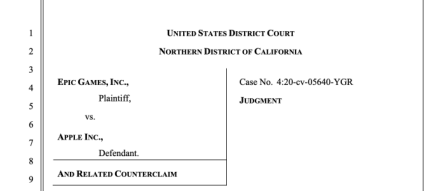

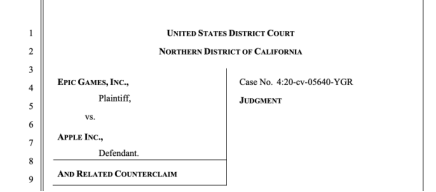

In 2021, game company Epic Games initiated an antitrust lawsuit against Apple. The U.S. District Court for the Northern District of California ruled that Apple had not violated antitrust laws, but also held that Apple must allow developers to place third-party payment links within their apps.

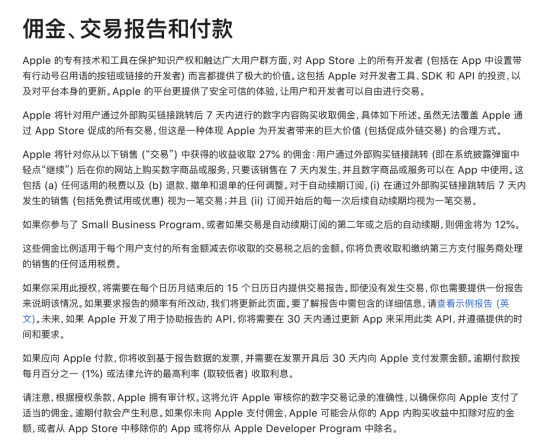

On January 17, 2024, Apple announced a series of adjustments to its App Store terms, allowing U.S. developers to provide external payment methods in their apps. However, Apple still charges developers high commissions and requires payment and transaction reports to be submitted within prescribed monthly deadlines.

Under the revised terms, the App Store charges a 27% fee on user purchases or annual subscriptions made through such links, only three percentage points lower than before. This marginal adjustment has been viewed by app developers as lacking sincerity. On March 20, 2024, Meta, Microsoft, X, and Match Group jointly sided with Epic Games and submitted documents to the court, protesting Apple’s deliberate circumvention of the spirit of the injunction.

3. Europe

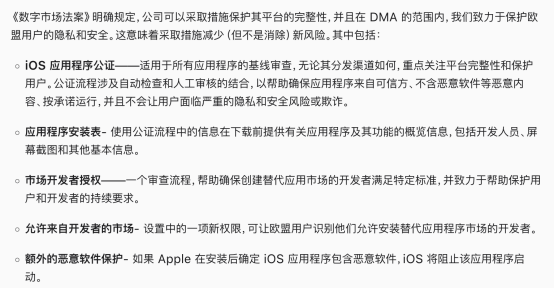

Pursuant to the requirements of the new Digital Markets Act (DMA), Apple released iOS 17.4 on March 6, 2024, for the first time opening app sideloading in the EU, allowing eligible developers to distribute apps via websites. Apple also imposed a series of requirements: distributed apps must comply with Apple’s review standards, and the website must be registered in App Store Connect. Developers eligible to distribute apps via the web must have been registered members of the Apple Developer Program in the EU for two consecutive years, and the app must have exceeded one million first-time installations in the EU in the previous year. After exceeding one million installations, Apple charges EUR 0.5 for each additional new user installation.

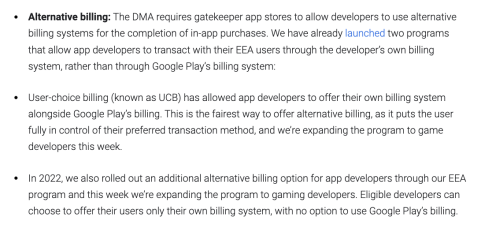

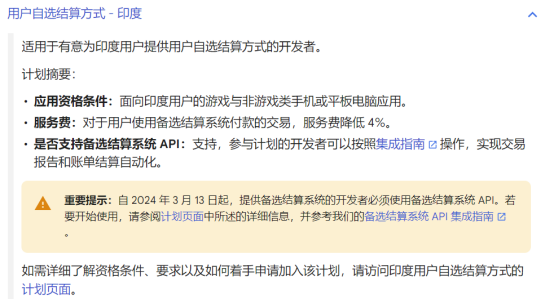

On March 5, 2024, Google also announced in its DMA compliance policy that it would allow game developers in the European Economic Area to provide external payment channels for purchases.

4. Japan

On December 26, 2023, according to Nikkei News, Japan is also preparing to introduce legislation requiring tech giants such as Apple and Google to allow external app stores to conduct payments on their mobile operating systems, in order to curb abuses of their dominant market positions. According to reports, the legislation restricting monopolistic conduct by Apple and Google is expected to be submitted to the Japanese parliament in 2024.

5. Other Regions

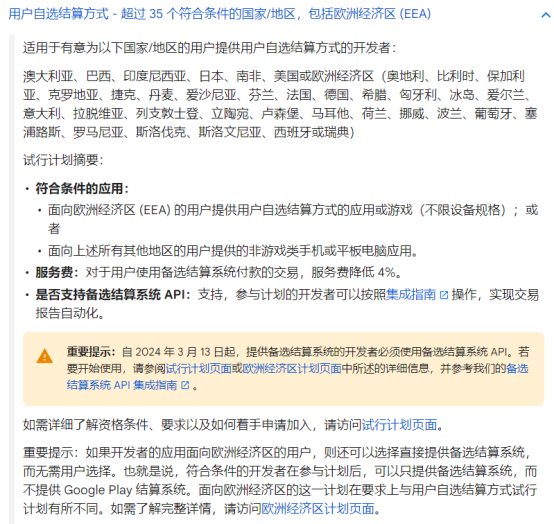

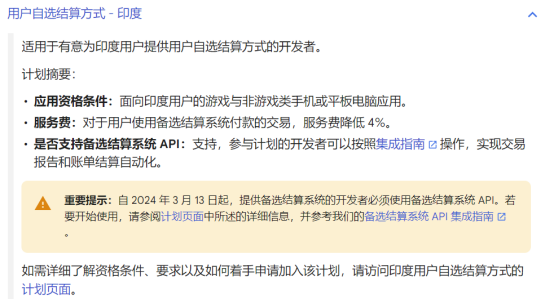

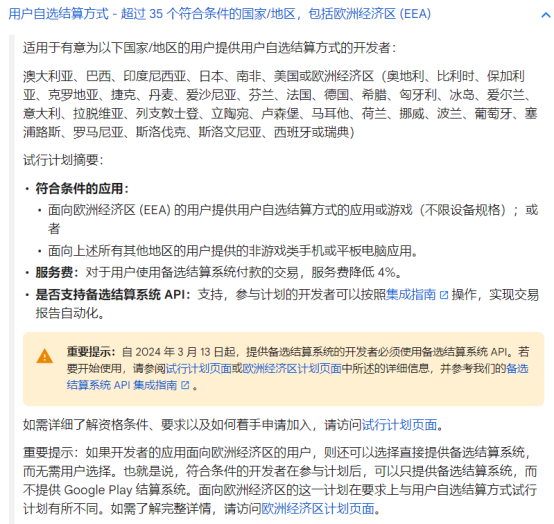

Since opening third-party payments in response to South Korean policy requirements in 2021, Google has gradually expanded its policies to more than 35 eligible countries or regions. However, at present, optional billing systems for game products are only available to users within the European Economic Area.

From the evolution of policies, the regulatory risk of directly integrating third-party payments within games remains relatively high. However, platform operators are continuously adjusting their payment policies in response to antitrust regulation across different regions, showing a gradual trend toward openness. Compared with strictly regulated third-party payments, official website payment has faced relatively fewer restrictions from Apple App Store and Google Play. With further loosening of platform policies regarding third-party payments and sideloading access, more operational space is expected to emerge.